ASC 606 Revenue Recognition Explained for SaaS Companies

5 Simple Financial Planning Tips Every Small Business Owner Should Know

January 21, 2026

How To Reduce Your Tax Bill! 10 Tips for Small Business Owners

January 28, 2026

Revenue is the heartbeat of any SaaS business. But how and when that revenue shows up on your books can change everything, from investor confidence to tax planning to long-term growth decisions. Many SaaS founders believe revenue recognition is simple because customers pay monthly or yearly. In reality, it is one of the most misunderstood areas of SaaS accounting.

ASC 606 Revenue Recognition was introduced to bring clarity and consistency across industries. For SaaS companies, it reshaped how subscription income, upgrades, discounts, and contracts are recorded. The rules are detailed, but they exist for a reason. They aim to reflect the true economic value a company delivers over time, not just when cash hits the bank.

In this guide, we break down ASC 606 Revenue Recognition in clear, simple terms. We focus specifically on SaaS models, real use cases, and practical decisions SaaS leaders face every day. If you want fewer accounting surprises and cleaner financials, this is essential reading.

Source: younium.com

What Is ASC 606 Revenue Recognition and Why It Matters

ASC 606 Revenue Recognition is a U.S. accounting standard issued by the Financial Accounting Standards Board. It defines how companies should recognize revenue from contracts with customers. Instead of industry-specific rules, ASC 606 uses a single, principle-based model.

For SaaS companies, this matters because revenue is often earned over time. Customers pay upfront for annual plans, receive free trials, or buy bundles that include support, setup, and usage-based fees. ASC 606 Revenue Recognition ensures revenue is recorded when the service is delivered, not just when payment is received.

This approach improves financial transparency. Investors, lenders, and buyers can better compare SaaS businesses. It also reduces the risk of inflated revenue numbers that do not match actual performance.

The Five-Step Framework Explained Simply

ASC 606 Revenue Recognition follows a five-step framework. Every SaaS company must apply these steps to customer contracts.

Step 1: Identify the Contract

A contract exists when both parties approve it, rights are clear, payment terms are defined, and collection is likely. For SaaS, this usually includes online subscriptions, master service agreements, or enterprise contracts.

Step 2: Identify Performance Obligations

A performance obligation is a promise to deliver a service. In SaaS, access to the software is usually one obligation. Setup, onboarding, training, or premium support may be separate if they provide distinct value.

Step 3: Determine the Transaction Price

This is the total amount the customer expects to pay. It includes fixed fees, usage-based charges, discounts, credits, and potential refunds. Variable pricing must be estimated carefully.

Step 4: Allocate the Price

If there are multiple performance obligations, the transaction price must be split based on stand-alone selling prices. This is where many SaaS companies struggle, especially with bundled plans.

Step 5: Recognize Revenue

Revenue is recognized when the service is delivered. For most SaaS subscriptions, this happens evenly over the contract term.

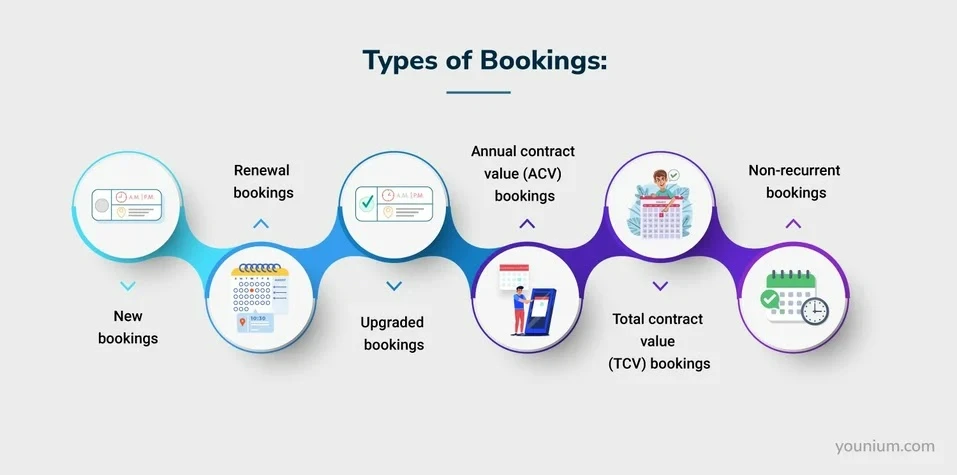

ASC 606 for SaaS Companies: Key Challenges

Here are some of the challenges SaaS companies face when it comes to ASC 606.

Subscription-Based Revenue

SaaS revenue is often recurring. Under ASC 606 for SaaS companies, annual or multi-year subscriptions cannot be recognized upfront. Revenue must be spread over the service period, even if cash is collected early.

Free Trials and Discounts

Free trials may delay the start of revenue recognition. Discounts and promotions affect the transaction price and must be allocated correctly.

Upgrades and Downgrades

Contract changes are common in SaaS. Upgrades, add-ons, or downgrades require reassessment under ASC 606 Revenue Recognition rules to determine if they create a new contract or modify an existing one.

Usage-Based Fees

Usage-based revenue is recognized when usage occurs. Estimating this accurately is critical for compliance.

SaaS Revenue Recognition ASC 606 Example

Let’s walk through a simple SaaS revenue recognition ASC 606 example.

A customer signs up for a one-year SaaS subscription at $12,000, billed upfront. The contract includes software access only.

Even though the company receives $12,000 on day one, ASC 606 Revenue Recognition requires recognizing $1,000 per month over 12 months. The remaining balance is recorded as deferred revenue on the balance sheet.

This method ensures financial statements reflect actual service delivery, not just cash flow.

Handling Bundled Services and Complex Contracts

Many SaaS companies bundle services such as onboarding, training, or priority support.

If onboarding is optional and provides distinct value, it may be a separate performance obligation. Revenue for onboarding could be recognized when the service is completed, while subscription revenue continues over time.

This is where detailed contract review becomes critical. Small wording changes can affect how revenue is split and recognized.

ASC 606 Revenue Recognition Examples in Real SaaS Scenarios

Here are a few common situations SaaS companies face:

- Annual subscription with a free setup fee waived as a promotion

- Multi-year contract with price increases in later years

- Enterprise deal with usage-based overage charges

- Subscription bundled with consulting hours

Each scenario requires applying the five-step model carefully. These ASC 606 revenue recognition examples show why automation and expertise matter. Manual tracking increases the risk of errors.

SaaS Revenue Recognition ADC 606 and Common Confusion

Many founders search for SaaS revenue recognition ADC 606 when they actually mean ASC 606. This confusion is common, especially among non-accounting teams.

Despite the typo, the underlying issue remains the same. SaaS revenue recognition ADC 606 searches usually reflect a need for clarity around deferred revenue, contract changes, and subscription accounting.

Understanding the correct standard and applying it consistently is far more important than terminology.

Why Accurate ASC 606 Revenue Recognition Protects Your Business

Correct ASC 606 Revenue Recognition is not just about compliance. It directly impacts:

- Financial reporting accuracy

- Investor trust and due diligence

- Valuation during fundraising or acquisition

- Audit readiness

- Forecasting and strategic planning

Poor revenue recognition can lead to restated financials, delayed funding rounds, and lost credibility.

Tools, Systems, and Internal Controls

Most growing SaaS companies cannot manage ASC 606 Revenue Recognition in spreadsheets alone. Subscription billing systems for recurring expenses, revenue recognition software, and clean contract data are essential.

Internal controls should include regular contract reviews, deferred revenue reconciliations, and clear documentation. These processes reduce errors and make audits smoother.

Getting ASC 606 Right in SaaS

ASC 606 Revenue Recognition is a long-term framework, not a one-time setup. As SaaS companies evolve, pricing models change, contracts get more complex, and expectations from investors rise.

By understanding the five-step model, applying it consistently, and learning from real SaaS revenue recognition ASC 606 example scenarios, SaaS leaders can avoid costly mistakes. Even commonly mis-typed searches like SaaS revenue recognition ADC 606 point to the same need for clarity and structure.

Strong ASC 606 for SaaS companies practices create cleaner books, better insights, and more confidence in decision-making. With real-world ASC 606 revenue recognition examples as guidance, compliance becomes manageable rather than overwhelming.

If you want expert support to implement and maintain ASC 606 Revenue Recognition without slowing down growth, we recommend working with Monily. We help SaaS companies simplify complex accounting, stay compliant, and gain clear financial visibility. Book a consultation with us.

Raza Agha

Raza Agha is a Senior Manager at Monily, specializing in global finance accounting and management. With a decade of experience, including roles as Accounting Manager and Assistant Manager at Health Grades Analytics, Raza drives financial efficiency and accuracy. He holds an MBA and Bachelor's degree in Accounting and Finance from The University of Texas at Austin and is a qualified ACA ICAEW and ACCA member. Based in Texas, Raza excels in strategic financial planning and operations.

{kind=link}

{kind=link}

{kind=link}